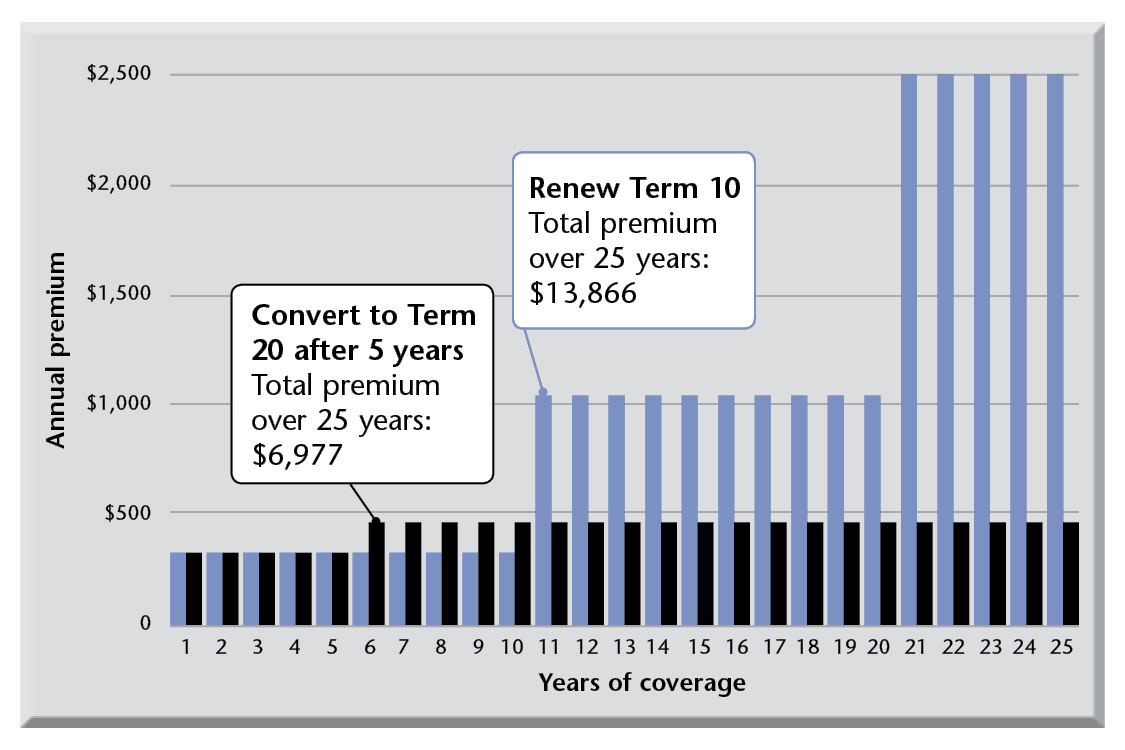

Stay on track to help achieve your investment goals

During times of economic and market turmoil, when the headlines bombard you and cause concerns, the advice of your financial security advisor is even more important. He or she can help guide you away from making investment decisions based on emotional reactions to headlines.

Although it’s disconcerting to see the value of your portfolio shift significantly, there are steps you can take to ride out market volatility and improve your confidence you’re still on track to achieve your investment goals.

Reaffirm your risk tolerance

By using a defined process that strategically designs an asset mix and selects the right combination of funds for you, your financial security advisor can reaffirm your tolerance for risk and verify your overall portfolio is correctly aligned with your investment needs.

Realign expectations

It’s important to use reasonable performance numbers when crafting your financial security plan because history has shown you can’t rely on a never-ending series of market gains. Working with your financial security advisor to find a conservative rate of return assumption can help keep short term fluctuations in perspective.

Rebalance your portfolio

Rebalancing makes sure you maintain the appropriate long-term asset mix recommended for your risk tolerance. Depending on your tolerance for risk you may need to change some of the investments within your portfolio to become more aggressive (using more equities) or more conservative (using more fixed-income products).

Reinvest in your plan

Don’t wait to invest. Down markets provide buying opportunities – consider the adage buy low, sell high – because some investments’ prices drop below their value.

During times of economic uncertainty and volatile markets, stay on track and avoid emotional reactions to headlines which can derail you from achieving your long-term investment goals.

Does participating life insurance have a place in your portfolio?

Understanding how different asset classes can be used to your advantage can be a big benefit when creating your financial security plan.

Would you consider life insurance and its cash value to be an important contributor to your net worth?

Consider participating life insurance as a unique asset class

Participating life insurance is a unique asset class because of its mix of immediate estate enhancement, cash value growth and the opportunity for life insurance benefit growth through dividends. This combination of benefits is a mix only offered with participating life insurance and can help you meet your financial goals.

Guaranteed cash value that won’t go down: Unlike most other assets that may be exposed to market volatility, participating life insurance has guaranteed cash values. And policyowner dividend values, once credited to a participating life insurance policy, can’t be reduced except as the policy or policyowner allows (for example, to help cover premiums). Accumulated values are fully protected from down-side market risk.

Tax advantages: While cash value is growing inside the policy, clients aren’t subject to tax on this growth (within legislative limits). And, the life insurance benefit passes tax free to your named beneficiary.

Flexibility: Whether your goal is estate preservation or having access to your policy’s cash value for retirement or other future needs, you have flexibility to help accomplish your personal financial goals.

Professionally managed: The participating account assets backing participating policies are usually managed by an experienced group of professionals.

The assets of the participating account are broadly diversified and the account is generally managed as a fixed-income account. There are specific teams of experts responsible for managing each asset class within the account’s portfolio.

Speak with your financial security advisor today about how you can benefit from adding participating life insurance to your financial security portfolio.

Why children need life insurance

Why would anyone buy life insurance for their children or grandchildren? For some people, it’s upsetting to even think about.

However, there are several scenarios where, in addition to the basic need for life insurance, it can make a big difference to a child’s future.

Helps build a nest egg

Consider the impact on your children’s start into adulthood if they could use the cash value of a permanent life insurance policy as a nest egg – to help pay for their education, as a down payment on their first home or to travel the world.

Compared with other investments, permanent life insurance can help you build a nest egg more tax-efficiently. While the cash value is growing inside the policy*, you’re not subject to tax on the growth, within prescribed limits. As a result of this tax advantage, more of your savings go towards your children’s future, instead of taxes.

When the children turn 18, you can transfer the ownership of the policy to them. They can simply let it grow or, when needed, access its cash value through withdrawals, surrender or borrowing.*

Ensures they can get protection as adults

Some life insurance policies offer options to guarantee your children’s future insurability – regardless of disability, illness, occupation, residency or foreign travel.

Without this, children who develop serious health problems *may not be able to get the financial protection they need when they grow up. Depending on the career they chose or where their travels take them, they may even be denied coverage. This may make it impossible for them to properly protect themselves and their family.

When you buy insurance with an option guaranteeing your children’s future insurability, you help protect them from these financial risks. If your children eventually have children of their own, then you are also helping to protect future generations.

Talk with your financial security advisor

Some people believe life insurance for children is unnecessary. For others, its special benefits (such as tax-advantaged growth and guaranteed insurability option) make it a valuable part of their family’s financial security plan. Talk with your financial security advisor to help decide what’s best for your children.

* Withdrawals will result in lower future values and possible tax implications. Any outstanding indebtedness reduces the death benefit.

The information provided is based on current laws, regulations and other rules applicable to Canadian residents. It is accurate to the best of the writer’s knowledge as of the date submitted for publication. Rules and their interpretation may change, affecting the accuracy of the information. The information provided is general in nature, and should not be relied upon as a substitute for advice in any specific situation. For specific situations, obtain advice from the appropriate legal, accounting, tax or other professional advisors. The views expressed are those of the author and not necessarily those of the issuer of any financial products for which the author may act as a distributor.

Changes to mortgage lending rules

The federal government has recently made several changes to mortgage lending rules. These changes could affect you if you’re looking at buying a home or refinancing.

Amortization period lowered

The maximum amortization period for a government-insured mortgage has been reduced to 25 from 30 years. While this move will monthly mortgage payments increase, it will also reduce the total interest you pay on a mortgage.

Here’s how it could work for you:

The following calculation* is based on a $300,000 mortgage with an interest rate of four per cent and an amortization period of 30 years.

|

Monthly payment |

Amortization |

Interest paid |

|

$1,426.56 |

30 years |

$213,558.84 |

The following calculation* is based on a $300,000 mortgage with an interest rate of four per cent and an amortization period of 25 years.

|

Monthly payment |

Amortization |

Interest paid |

|

$1,578.06 |

25.10 years |

$173,418.23 |

* This calculation is an approximation; this is not an approved amount. Actual mortgage applications are subject to approval and London Life lending criteria. Calculated on June 25, 2012.

In this example, you would save $40,141 in interest while your monthly payment would be $152 higher.

New limits on refinancing

The maximum you can refinance against your home also has dropped – to 80 per cent of its value

from 85 per cent. This reduces the amount of equity you may borrow against for such things as

debt consolidation and renovations.

Changes to service ratios

Under the new rules, you can spend up to 39 per cent of your gross debt service ratio on home expenses such as your mortgage, property taxes and heating. You can spend up to 44 per cent of your total debt service ratio on housing expenses and all other debt. This may or may not impact your borrowing ability depending on whether a lender’s maximum gross debt service ratios already fall within these requirements.

Government-backed insured mortgages now are limited to home purchases of less than $1 million. A down payment of at least 20 per cent now is required on mortgage loans for homes priced at $1 million or more.

These new rules took effect July 9.

Download a PDF of Your Financial Security, Issue 3, 2012